[ad_1]

The sharp falloff in bank card utilization throughout the coronavirus recession has introduced forth an attention-grabbing mix of innovation in product design, worth propositions that depend on shoppers’ hopes for a return to some semblance of the “outdated regular,” and renewed reliance on junk mail, that decades-old standby of card promotion.

It’s as if the very plastic a lot of the playing cards are product of was getting recycled into one thing that appears like the standard card, however that’s coming to be greater than that.

This is available in a interval the place shoppers have grown sad with features of the bank card enterprise by means of a lot of the pandemic and the ensuing financial droop. Their spending patterns modified drastically out of necessity and lack of alternative.

New Entrants with a Retro Angle to Them

A style of what’s happening might be seen in two revolutionary card introductions.

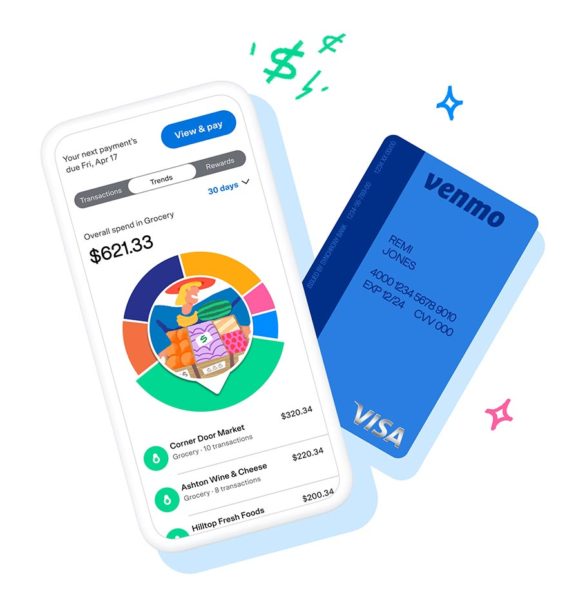

• Venmo, the digital person-to-person fee service that has vied with the banking trade’s challenger, Zelle, gave its new Venmo Credit score Card a tender launch for choose customers of the service.

Working with Synchrony Financial institution, Venmo launched a fee automobile that’s acquired one thing of all the things. It personalizes its cashback function to reward customers with its prime price of three% again in their very own prime spending class, and decrease cashback charges for different spending. It permits cardholders to pay through two strategies that remove or decrease contact — a novel QR code on the cardboard and an RFID-enabled chip that allows faucet and go transactions. The cardboard might be managed immediately within the Venmo app, together with transaction alerts and freezes, and the cardboard can be utilized in Venmo P2P funds — even money rewards might be despatched to buddies. On-line buying might be accomplished with a digital card even earlier than the bodily card is delivered. Chosen Venmo customers can apply by means of their app.

• Lodges.com and Wells Fargo launched a Lodges.com Rewards card that options “rewards that rework on a regular basis spending into extra rewarding journey.”

Journey? Now?

The brand new effort just isn’t the primary program throughout the pandemic to emphasise journey rewards. The cardboard’s rewards program ties into the web site’s preexisting program that turns “stamps” for lodge stays into free lodge nights. The cardboard will flip spending into stamps.

Innovation is growing as issuers have began to find out that COVID-19 will likely be with us for a while, based on Andrew Davidson, SVP/Chief Insights Officer at Comperemedia, a Mintel firm. “We’re seeing this throughout the spectrum,” he continues. “Card corporations have determined to not maintain again on concepts and packages any longer.” Greater than a dozen new packages, many that includes collaboration between issuers and nonbank corporations, have been unveiled as competitors heats up.

The digital gorilla within the room is the Apple Card, which has been enjoying its playing cards properly throughout the recession. “The Apple Card’s worth proposition has develop into stronger and stronger,” says Davidson, because it provides extra companions to its cashback program. Apple and its companions have been emailing closely throughout the pandemic to drive signups and utilization. Apple rolled out useful lodging early within the pandemic, together with an outbound provide on cell gadgets for aid that required just one button to be pushed. Many different issuers adopted, some making aid simpler to acquire than others, however Apple stole the scene.

“They have been first out of the gate, when it comes to serving to clients,” says Davidson. And this comes at a time when analysis by J.D. Energy signifies that many shoppers have been pissed off or dissatisfied with their card issuers. “U.S bank card clients look like dropping religion that their card issuers will likely be right here for them after they want it most because the COVID-19 pandemic continues to pull on client confidence,” the agency acknowledged in publishing its annual bank card satisfaction research.

Let’s check out the headwinds card issuers are dealing with, first, after which at how card entrepreneurs have been adapting to altering circumstances.

Learn Extra:

Shoppers Have Been Slicing Again and Shifting Spending

In early October 2020 the Federal Reserve reported that U.S. revolving credit score had fallen in August at an annualized price of 11.three%. Whole excellent revolving credit score, at $1.08 trillion on the finish of the primary quarter of 2020, had fallen to $985.three billion in August, a period-to-period lower of eight.6%.

“Shoppers nonetheless assume the worst is but to return, financially.”

— John Cabell, J.D. Energy

“Shoppers nonetheless assume the worst is but to return, financially,” says John Cabell, Director of Banking and Cost Intelligence at J.D. Energy. “Folks have gotten extra miserly with their playing cards, spending much less and paying them off.”

Davidson agrees: “The fallout hasn’t actually taken maintain but.”

Cabell says that earlier than the pandemic, 44% of shoppers within the Powers samples have been carrying a steadiness and 56% have been paying their payments in full each month. Publish-pandemic, he says, 39% have been carrying a steadiness and 61% have been paying off their balances. Folks have additionally modified what they use their playing cards for, with groceries, pharmacy fees and takeout eating now.

Cabell notes that a rising proportion of the nation’s jobs haven’t solely gone, however received’t be again for the foreseeable future. Within the face of accelerating financial uncertainty and worse, the outlook for the cardboard enterprise isn’t promising. In a abstract of a Mercator Advisory Group report on the cardboard setting, Brian Riley, Director, Credit score Advisory, states: “Bank cards are definitely not going away, however anticipate decrease returns, increased dangers and shifting buy patterns at the least by means of 2025.”

Banking remodeled webinar

How To Compete With the Large Banks on a Restricted Advertising Funds

Be part of Jim Marous and James Robert Lay as they focus on unlock the secrets and techniques of a digital content material advertising and marketing technique that may yield 10X extra loans and deposits.

Tuesday, October 20th at 2pm est

Right now’s Card Economics

Although card rates of interest have come down a bit, Cabell and Davidson observe that they continue to be fairly excessive in comparison with different market charges and that this may increasingly proceed for a time. Riley states flatly that “Lending is a risk-based enterprise; it requires a return for tolerating the danger.” Whereas beneath sure circumstances shoppers can pay what they have to to maintain bank card strains open for survival, that is usually unsecured credit score, versus mortgages and auto loans.

The economics transcend rate of interest spreads. Cabell says most shoppers really feel they need to be getting one thing for his or her bank card transactions — factors, nights, miles, cashback or in any other case.

“The juiciest packages are inclined to have increased charges however these are in a state of flux.”

The juiciest packages are inclined to have increased charges however these are in a state of flux. Throughout the first a part of the pandemic many added extra variations on rewards to make up for the truth that folks couldn’t or wouldn’t journey. Davidson says a shift has begun again in direction of journey incentives, just like the Lodges.com card, and American Categorical and Hilton have added to the perks of their co-branded card even because the megachain introduced the everlasting closing of its Instances Sq. New York lodge.

“They’re having an eye fixed towards the longer term,” says Davidson, and relying on the affect of pent-up urge for food for journey. “I discover increasingly corporations are pondering longer-term.”

“Shoppers have many private monetary points and as card utilization modifications when it comes to kind and spending and other people journey much less, high-fee playing cards that provide previously enticing perks and advantages are doubtlessly going to develop into much less satisfying,” says Cabell. “Playing cards with account charges might develop into much less enticing down the street, and shoppers might migrate to no-fee playing cards.”

But Riley factors out that reward program prices already eat up a lot of the interchange earnings that issuers nonetheless get. “In a shifting market, all prices should obtain consideration,” says Riley.

J.D. Energy analysis signifies that, at current, shoppers generally tend to stay with the playing cards they’ve and plenty of aren’t on the lookout for extra card accounts. “They’re hanging onto what’s of their wallets now,” says Cabell.

However this might shift.

Cardholders Disillusioned with Issuers’ COVID Efficiency

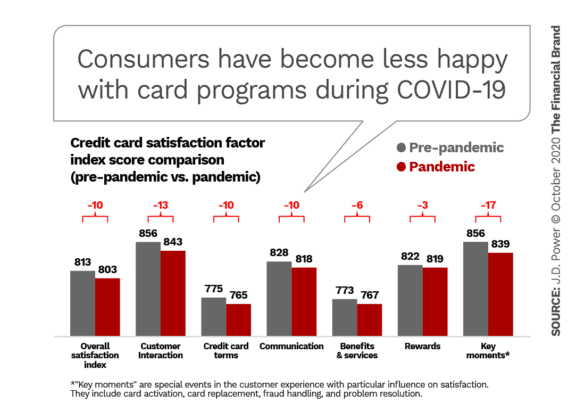

Certainly, there’s good purpose to assume that extra card account switching might come. J.D. Energy’s analysis signifies that many shoppers should not pleased with the way in which their issuers behaved early within the pandemic.

Because the findings within the chart above present, the weakest hyperlinks haven’t been in issues like reward packages, however fundamentals of customer support in a time of excessive stress. Distinction that with the phrase of mouth that the Apple Card’s outreach talked about earlier has garnered.

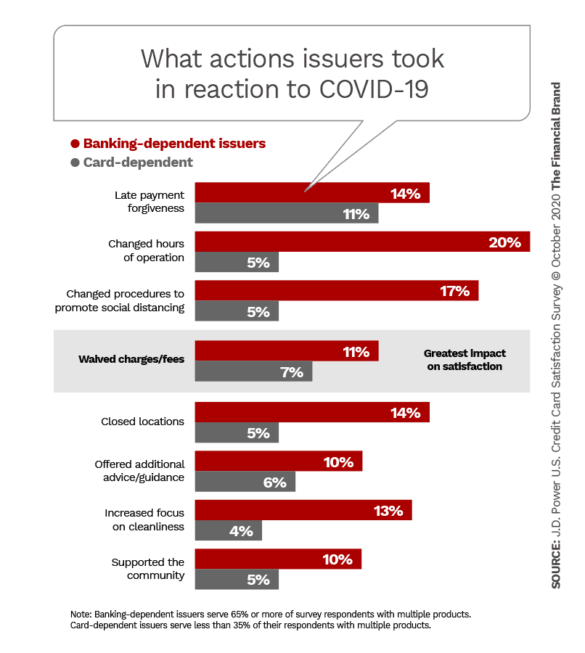

When it comes to concrete actions taken, whereas some issuers took the steps outlined within the chart beneath, many didn’t. The one which J.D. Energy recognized as being most significant to shoppers — waived fees and charges — have been granted by comparatively few issuers. Notice that each the Venmo and Lodges.com playing cards lined in the beginning of this text are no-fee choices.

Cabell notes that 2020 card satisfaction ranges, general, appeared pointed in direction of report ranges in January and February 2020. “However that each one reversed course when COVID-19 entered the equation, with satisfaction, belief, advocacy and model picture attributes leading to sharp declines.”

Cabell believes holding onto accounts in the long run will demand massive enchancment in communication with disgruntled clients. E-mail is the popular channel for this, however sturdy communication by means of all digital channels is rising in significance and name middle effectivity is at a premium.

Curiously, the strongest impression has been seen on the extremes — the prosperous and mass prosperous client segments and amongst these financially hit by the pandemic. J.D. Energy discovered that mainstream banking and mortgage lenders are seen as rather more proactive in speaking with shoppers throughout the pandemic than are card issuers.

[ad_2]

{kind=link}

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.